What Is a Personal Loan?

A personal loan is a fixed amount of money borrowed from a bank, credit union, or online lender that you repay in equal monthly installments over a predetermined period — typically between two and seven years. Unlike credit cards, which offer a revolving line of credit, a personal loan gives you a single lump sum with a clear payoff date.

Most personal loans are unsecured, meaning they don’t require you to put up collateral like your home or car. Instead, the lender evaluates your creditworthiness — your credit score, income, and financial history — to determine whether to approve you and at what interest rate.

Key Takeaway: Personal loans offer predictable, fixed monthly payments, which makes budgeting straightforward compared to variable-rate debt like credit cards.

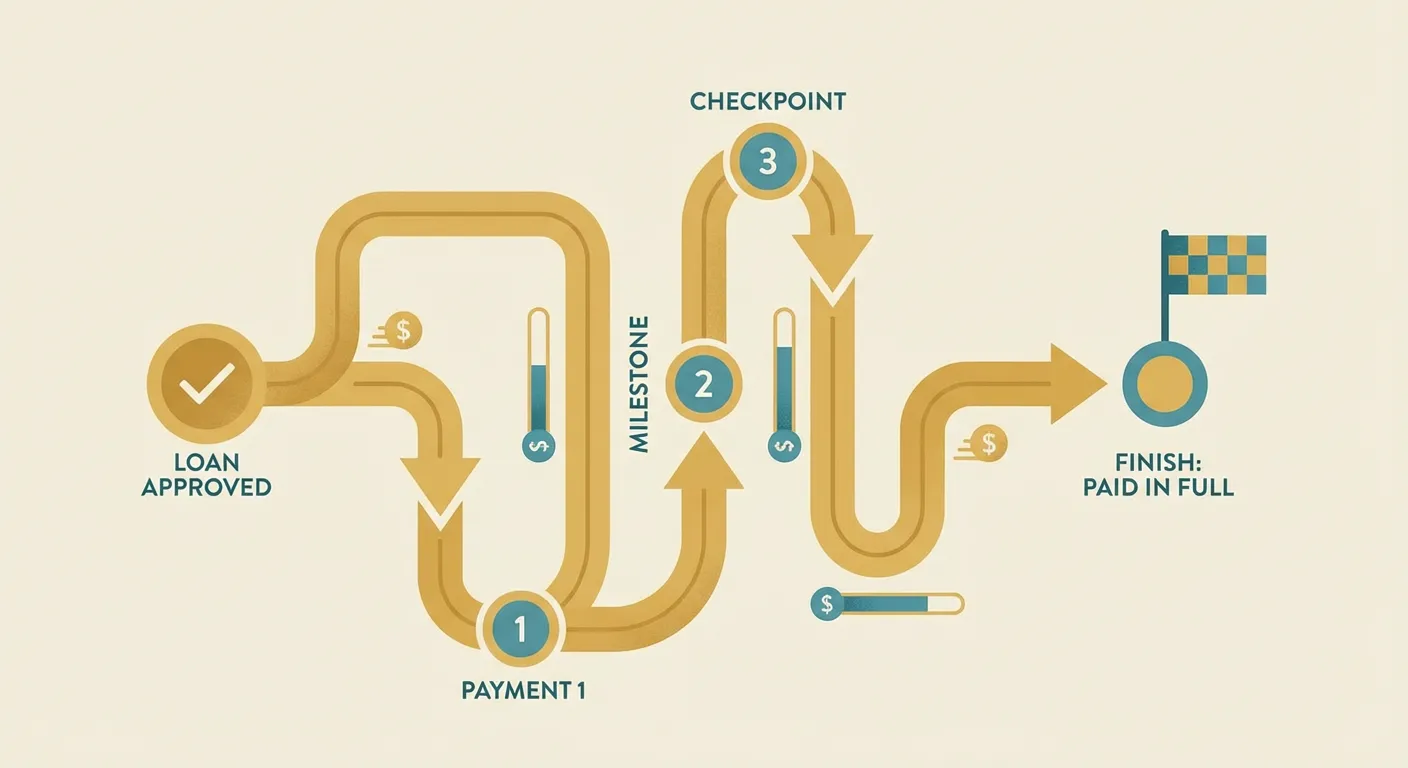

How Personal Loans Work

The mechanics of a personal loan are relatively simple, but understanding each step helps you make informed decisions.

1. Application and Approval You submit an application with personal and financial information. The lender reviews your credit profile, income, existing debts, and employment history. Many lenders offer prequalification with a soft credit pull that won’t affect your score.

2. Funding Once approved, the lender disburses the full loan amount — often within one to five business days. Some online lenders can fund within 24 hours.

3. Repayment You make fixed monthly payments that include both principal and interest. Each payment reduces your balance until the loan is fully repaid at the end of the term.

4. Completion Once you’ve made all scheduled payments, the loan is closed. There’s no ongoing obligation, and the account is reported as paid in full to the credit bureaus.

Common Uses for Personal Loans

Personal loans are versatile. Here are the most common reasons people take them out:

-

Debt consolidation — Combining high-interest credit card balances into a single, lower-rate payment. This is the most popular use case, accounting for nearly a third of all personal loans.

-

Emergency expenses — Covering unexpected medical bills, urgent home repairs, or other financial emergencies when savings fall short.

-

Home improvements — Funding renovations, repairs, or upgrades that can increase property value. Unlike a home equity loan, no collateral is required.

-

Major life events — Weddings, relocations, or other significant one-time expenses that benefit from structured repayment.

-

Medical procedures — Elective procedures or medical costs not fully covered by insurance.

What Lenders Evaluate

Understanding what lenders look for helps you prepare and potentially secure better terms.

Credit Score Your credit score is the single most influential factor. Scores above 670 generally qualify for competitive rates. Scores above 740 typically access the best terms available. Borrowers with scores below 580 may still find options but should expect higher rates.

Debt-to-Income Ratio (DTI) This measures how much of your gross monthly income goes toward existing debt payments. Most lenders prefer a DTI below 36%, though some will approve borrowers up to 50%.

Income and Employment Stable, verifiable income reassures lenders you can handle the payments. Most require at least two years of employment history, though some are more flexible for self-employed borrowers.

Credit History Length A longer track record of responsible borrowing works in your favor. Lenders want to see a pattern of on-time payments and responsible credit management.

Understanding Interest Rates and APR

The interest rate is what the lender charges to borrow money. The APR (Annual Percentage Rate) includes the interest rate plus any fees, giving you the true cost of borrowing.

Personal loan APRs typically range from 6% to 36%, depending on your credit profile and the lender. Here’s a general breakdown:

- Excellent credit (740+): 6% – 12% APR

- Good credit (670–739): 12% – 18% APR

- Fair credit (580–669): 18% – 28% APR

- Poor credit (below 580): 28% – 36% APR

Important: Always compare the APR, not just the interest rate. A loan with a low interest rate but high origination fees may cost more overall.

Fees to Watch For

Beyond interest, several fees can affect the total cost of your loan:

-

Origination fees — A one-time charge (typically 1% – 8% of the loan amount) deducted from your disbursement or added to your balance.

-

Late payment fees — Charged when you miss a payment deadline. Many lenders offer a grace period of 10–15 days.

-

Prepayment penalties — Some lenders charge a fee if you pay off the loan early. Many modern lenders have eliminated this fee, but always verify.

-

Returned payment fees — If a payment bounces due to insufficient funds.

Five Questions Every Borrower Should Ask

Before committing to any personal loan, get clear answers to these questions:

-

What is the total cost of the loan? Add up all payments over the full term, including fees. This is the true price of borrowing.

-

Is the rate fixed or variable? Fixed rates provide payment certainty. Variable rates may start lower but can increase over time.

-

Can I pay it off early without penalty? If your financial situation improves, you want the flexibility to eliminate the debt ahead of schedule.

-

What happens if I miss a payment? Understand late fees, grace periods, and the impact on your credit report.

-

How will this affect my credit? The initial application may cause a small, temporary dip. On-time payments will build your score over time.

When a Personal Loan May Not Be the Best Choice

Personal loans aren’t the right tool for every situation. Consider alternatives if:

- You only need a small amount (under $1,000) — a credit card with a 0% intro APR may be more cost-effective.

- You have home equity — a home equity loan or HELOC typically offers lower rates.

- Your credit score is very low — you may be better served by working on credit improvement first.

- The expense is discretionary — borrowing for wants rather than needs can create unnecessary financial strain.

This guide is for educational purposes only. VictoryLoans.com is an independent educational resource — not a lender, bank, or financial advisor. Always consult with a qualified professional regarding your specific financial situation.